How the world’s new megacities could present opportunities for investors

- 20 Septiembre 2021 (5 min read)

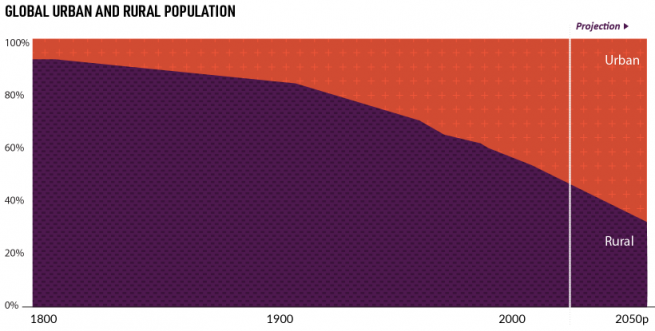

Presently more than half the world’s population, at 55%, lives in cities, up from just 30% in 1950. However by 2050, this figure is expected to soar to 70% - which translates to an estimated 2.5 billion more people migrating to urban areas over the next 20 years1 .

This trend has been driven by rapid urbanisation, as mass migration towards cities started in the years following the Industrial Revolution. As crop yields fell and there was less demand for manual farm labour, people migrated to cities in search of higher paid jobs by working in factories that produced consumer goods on a massive scale. But it wasn’t until 2007 that the portion of the global population living in cities exceeded the total living in rural areas (see chart below). This dramatic growth has resulted in the emergence of a number of megacities - defined as an urbanised centre with 10 million or more inhabitants - across the world.

- VU4gV29ybGQgVXJiYW5pemF0aW9uIFByb3NwZWN0cyAoMjAxOCk=

Emerging markets will dominate megacity growth

There are currently 33 megacities in the world2 , and as one might expect this contains the likes of New York, London and Paris. However, the list also heavily features emerging markets, with megacities in China and India in particular, and other notable examples that have experienced dramatic growth. Colombia’s Bogota, for example, gained 3.6 million people between 2000 and 2016, while the population in Lagos, Nigeria, doubled to nearly 14 million people over the same period3 .

We believe that developing nations are likely to dominate megacity growth over the next decade. For example, Jakarta, Indonesia, is projected to be the world’s largest megacity by 2030, while in Africa, the population of Angola’s largest city, Luanda, is forecast to increase by 60%. However, these countries will not just experience a surge in their respective populations; they will also likely benefit from huge economic growth. Cities such as Dhaka (Bangladesh), Manila (Philippines) and Bangalore (India) are all expected to exhibit close to 150% GDP growth by the end of the decade, and in 2030 there are expected to be 39 megacities contributing 15% of global GDP4 .

- RXVyb21vbml0b3IgSW50ZXJuYXRpb25hbCAoMjAxNyk=

- VW5pdGVkIE5hdGlvbnMgKDIwMTYp

- RXVyb21vbml0b3IgSW50ZXJuYXRpb25hbCAoMjAxNyk=

If we look even further ahead to the year 2050, it is projected that the landscape of megacities will be dominated by emerging market countries. This urbanisation trend is expected to be predominantly focused in Asia and Africa, with India, China and Nigeria alone expected to add a combined one billion to the global urban population.

Urbanisation drivers

Urbanisation occurs for socioeconomic reasons, with economic pull-factors particularly strong in emerging markets as an increase in the standard of living has the potential to lift millions out of poverty. In addition, large cities can provide additional advantages – and potential opportunities for investors.

First, local concentration of industry as companies flock to these populous areas. This has significant advantages such as low transport costs, a strong local market and a large supply of labour. All these factors can lead to potentially greater returns on capital and potentially higher profits for companies. For example, Delhi is one of India’s most productive metro areas, and we expect its services sector to continue to drive the city’s rapid economic growth.

Second, the potential for technological innovation. As the companies that make up an industry concentrate in a single area, they accumulate even more information and create local specialisation. This allows them to help direct the flow of new and innovative ideas, and potentially increase financial returns. For example, Shenzhen and Bangalore are prime technology hubs with top-class talent pools, encouraging start-up growth and expansion in their respective countries, and are potentially attractive to investors.

Building a new generation of cities

A key aspect of urbanisation will be a new generation of cities with smarter functionality, as well as next-generation infrastructure and services. In a more sustainability-focused world, characteristics like smarter utilities, car-sharing, digital healthcare systems, greener buildings and transport infrastructure should feature in new megacities. This could create a wealth of potential new opportunities for investors. What’s more, monitoring environmental, social and governance (ESG) factors and engagement by both international financial institutions and investors is crucial to collectively achieving a sustainable model.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2021 AXA Investment Managers. All rights reserved