EM Latin America reaction: Mexico keeps policy rate on hold at 11%

- 09 Mayo 2024 (3 min read)

First pause in the easing cycle

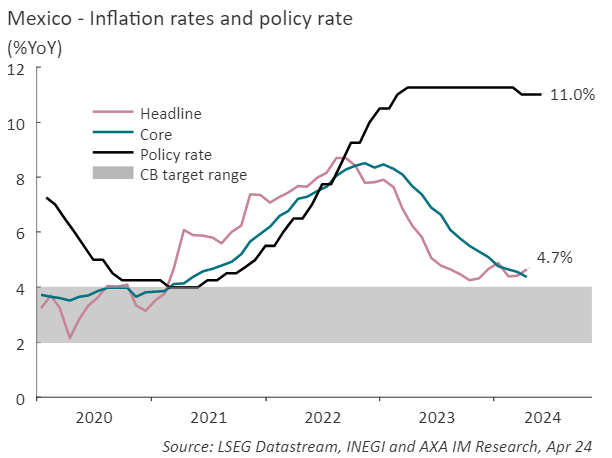

In line with expectations, the Bank of Mexico (Banxico) maintained its policy rate at 11% in a unanimous vote at its May monetary policy meeting. This decision marks the first pause in the easing cycle, as Banxico had suggested might occur, albeit coming at a very early stage. The easing cycle began just one meeting ago in March with a 25-basis point cut. The exchange rate and Mexican local rates remained relatively stable after the decision, indicating that the market had already priced in Banxico’s decision to pause.

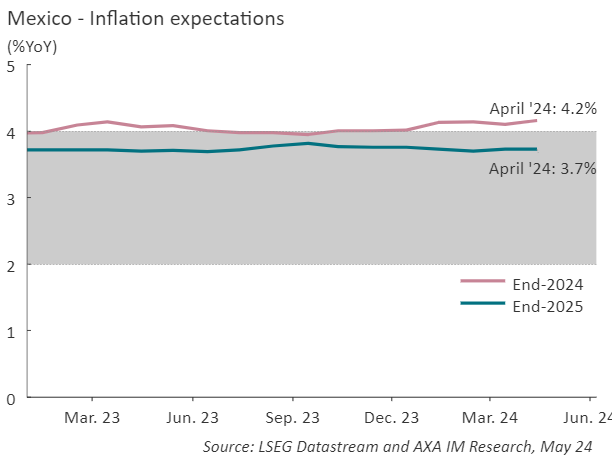

Despite the uptick in headline inflation observed since the last policy meeting (April: 4.7%), Banxico acknowledged in its statement that this increase primarily stemmed from the non-core component. It also noted, with approval that core inflation continued its downward trend, reaching 4.4% in April. In this context, the central bank stated its expectation for the ongoing disinflationary process to persist. However, the Board expressed concerns about the stickiness of services inflation, leading to an adjustment in its 2024 inflation forecast. It was revised slightly upwards to 4.0% from the previous 3.9%. Conversely, the 2025 forecast was revised downward by 0.1 percentage points to 3.0%. Additionally, Banxico postponed the timeline for inflation convergence to its 3% target. Now, it expects this convergence to occur in Q4 2025 instead of Q2 2025, as stated at their previous meeting. We envisage a similar trajectory for inflation this year (4.0%) and a higher rate (3.5%) for 2025.

Regarding the Mexican economy, the Board emphasized that the economic softness observed towards the end of 2023 likely persisted into early 2024, despite the labour market's resilience. This outlook aligns with preliminary estimates of Q1 GDP, which showed growth decelerating to 1.6% year-on-year from 2.5% in Q4, the slowest expansion since Q1 2021. We foresee growth continuing to slow throughout the rest of the year due to factors such as high interest rates, a decelerating US economy, and a decrease in remittances in pesos, reflecting the strength of the local currency. Nonetheless, increased public spending ahead of June’s general elections, alongside easing inflation and robust labour market conditions, are expected to provide some support. All things considered, we see growth moderating to 2.2% this year and edging down further to 2.1% in 2025.

Banxico, as in its previous meeting, refrained from offering explicit forward guidance in its policy statement. Instead, it indicated that it will "assess the inflationary outlook to discuss adjustments to the reference rate" in the future. This underscores the bank's commitment to remaining data-dependent. The Board also emphasized that, with this decision, the monetary policy stance remains restrictive. We expect Banxico to resume its easing cycle in June, following an approach of cutting rates at every other meeting. We see the policy rate reaching 10.25% by the end of this year and 7.50% by the close of 2025.

Related articles

View all articles

ECB Review: No commitment, no guidelines, no…thing

- by ,

- 19 Julio 2024 (3 min read)

UK reaction: In the right direction

- by

- 18 Julio 2024 (3 min read)

UK reaction: Still at target, but services remains sticky.

- by

- 17 Julio 2024 (3 min read)

EM Latin America reaction: Growth losing steam

- by

- 15 Abril 2024 (3 min read)

US reaction: Payrolls stay strong

- by

- 05 Abril 2024 (5 min read)

Disclaimer

Este documento ha sido emitido por AXA IM México, S.A. de C.V., (“AXA IM Mexico”) un asesor financiero independiente constituido de conformidad con la Ley del Mercado de Valores. La información aquí contenida es consistente con las disposiciones contenidas en el artículo 6 de la Ley del Mercado de Valores, de conformidad con las disposiciones del Artículo 226, Sección VIII del mismo ordenamiento legal.

Este documento y la información contenida en este documento están diseñados para el uso exclusivo de clientes sofisticados o inversionistas institucionales y/o calificados y no debe ser dirigido hacia clientes minoristas o inversionistas particulares. Ha sido preparado y publicado con fines informativos únicamente a solicitud exclusiva de los destinatarios especificados y no destinado a la circulación general entre el público inversionista. Es estrictamente confidencial y no se debe reproducir, distribuir, circular, redistribuir ni utilizar de otra manera, total o parcialmente, de ninguna manera sin el consentimiento previo por escrito de AXA IM Mexico. No está destinado a ser distribuido a ninguna persona o jurisdicción para la que esté prohibido.

En la medida de lo permitido por la ley, AXA IM Mexico no garantiza la exactitud o idoneidad de cualquier información contenida en este documento y no asume responsabilidad alguna por errores o declaraciones erróneas, ya sea por negligencia o cualquier otra razón. Dicha información puede estar sujeta a cambios sin previo aviso. Los datos contenidos en este documento, incluyendo pero no limitado a cualquier backtesting, historial de desempeño simulado, análisis de escenarios e instrucciones de inversión, se basan en una serie de supuestos e insumos clave y se presentan con fines indicativos y / o ilustrativos solamente.

Este documento ha sido preparado sin tener en cuenta las circunstancias personales específicas, los objetivos de inversión, la situación financiera o las necesidades particulares de persona alguna en particular. Nada de lo contenido en este documento constituirá una oferta para entrar o un término o condición de cualquier negocio, transacción, contrato o acuerdo con el receptor del mismo o con cualquier otra parte. Este documento no se considerará como asesoría en inversión, asesoría fiscal o legal, ni una oferta de venta o solicitud de inversión en un fondo en particular. Si no está seguro del significado de cualquier información contenida en este documento, consulte a su asesor financiero u otro asesor profesional. Los datos, las proyecciones, los pronósticos, las previsiones, las hipótesis y / o las opiniones aquí vertidas son subjetivos y no son necesariamente utilizados o seguidos por AXA IM Mexico o sus compañías afiliadas que pueden actuar basándose en sus propias opiniones y como áreas independientes dentro de la organización.

Toda actividad de inversión conlleva riesgos. Debe tener en cuenta que las inversiones pueden aumentar o disminuir en valor y que el rendimiento pasado no es garantía de rentabilidades futuras, es posible que no reciba la cantidad inicialmente invertida. Los inversores no deben tomar ninguna decisión de inversión basada únicamente en este material.

Si algún fondo se destaca de manera particular en esta comunicación (el "Fondo"), su documento de oferta, prospecto de inversión o documento de información clave contiene información importante sobre restricciones de venta y factores de riesgo, debe leerlos cuidadosamente antes de realizar cualquier transacción. Es su responsabilidad conocer y observar todas las leyes y reglamentos aplicables de cualquier jurisdicción pertinente. AXA IM Mexico no tiene intención de ofrecer ningún Fondo en ningún país donde dicha oferta esté prohibida.

Para conocer la totalidad de los riesgos asociados, lea cuidadosamente el prospecto y/o el folleto de información clave del fondo.

AXA IM México, S.A. de C.V. está inscrita en el Registro Público de Asesores en Inversiones con número de folio 30054-001-(14084)-20/05/2016, asignado por la Comisión Nacional Bancaria y de Valores. Al respecto, la Comisión Nacional Bancaria y de Valores supervisa exclusivamente la prestación de servicios de administración de cartera de valores cuando se tomen decisiones de inversión a nombre y por cuenta de terceros, así como los servicios consistentes en otorgar asesoría de inversión en Valores, análisis y emisión de recomendaciones de inversión de manera individualizada, por lo que dicha Comisión Nacional Bancaria y de Valores carece de atribuciones para supervisar o regular cualquier otro servicio que AXA IM México pueda proporcionar a sus clientes. La inscripción en el Registro Público de Asesores en Inversiones que lleva la Comisión Nacional Bancaria y de Valores en términos de la Ley del Mercado de Valores, no implica el apego de AXA IM México a las disposiciones aplicables en los servicios prestados, ni la exactitud o veracidad de la información proporcionada.

AXA IM México, S.A. de C.V. conforme a la Ley del Mercado de Valores, tiene prohibido garantizar rendimientos a sus clientes sobre sus inversiones, así como recibir en depósito o custodia dinero o valores de sus clientes.

Asimismo, AXA IM México no percibe remuneraciones de parte de emisoras o personas relacionadas por la promoción de valores, ni de intermediarios del mercado de valores, nacionales o del extranjero.